Over the last two financial years the central office of the

Shop Distributive and Allied Employees Association (SDA) made over 4.3 million

dollars in profit. This is at a time when most unions have been losing money as

they struggle with declining membership. Flipping through the asset listing on

the SDA’s balance sheet, it’s hard to remember that this is a union for some of

the lowest paid workers in the country, and not some large private hedge fund.

The SDA has always been a bit unique. Despite representing a

largely young and mostly female workforce of checkout and retail workers, the

union has been vocal within the Australian Labor Party campaigning on a

conservative Christian platform against abortion and gay marriage. One of the

original anti-communist unions in Australia, the SDA is also known for taking a

non-combative negotiating approach when talking to businesses, winning the

dubious honour of being the only union that has been praised by Eric Abetz.

More recently, the SDA has come under criticism for deals

struck with major employers that appeared to be too soft on the companies

involved, with workers losing penalty rates and overtime in exchange for

minimal increases in their hourly pay. Fair Work Australia found that workers

with more weekend and night shifts were actually worse off under these deals.

Considering the whole purpose of a union is to gain better working conditions

for its workers, this finding raised serious questions about the credibility of

the SDA.

Despite the controversy the SDA has attracted over the last

six months, it doesn’t seem to have effected their bottom line. The

4.3-million-dollar central office profit from the last 48 months came off

revenue of just 18.3 million, giving the central office a profit ratio of over

22%. Most companies would kill for margins like that. To put these figures in

perspective, the Construction Forestry Mining and Energy Union (CFMEU) central

office posted a loss of $433,256 over the last two reported years, the

Australian Workers Union (AWU) central office lost 1.36 million and even the

Australian Nursing and Midwifery Foundation (ANMF), one of the only unions

increasing in members made a small loss.

For a Not-for-Profit organization to be making profits like

this is pretty strange. The basic long term financial principal for this type

of organization is to break even, while ensuring you have enough money in the

bank for a rainy day. While you want to save some money, overall your revenue

should be close to matching your expenses to ensure you are doing as much as

you can while at the same time not charging members more fees than you need to.

The SDA central office doesn’t seem be run per these principles. In February

2015, the same financial year the national organization made a profit of over 4

million the SDA released a press release stating that they needed to increase

their membership fees as their costs had gone up. You do have to wonder how

those same members would have felt a couple of months later if they looked at

the annual report of the national office. It’s not as if these profits were a

one off either. The central office has built up an impressive amount of equity

on its balance sheet; 26.7 million in term deposits, an 18.5 million-dollar

portfolio of investment property, far more than any other union I could find.

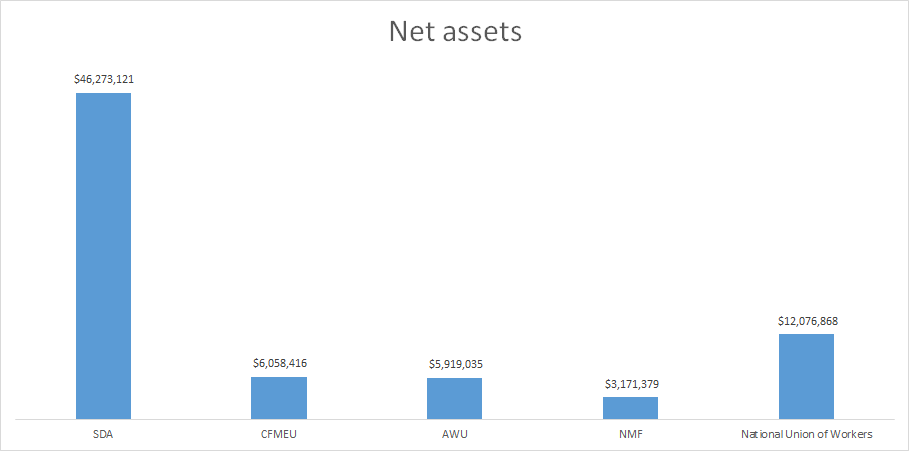

The below graph compares the net balance sheet position of some of the national

offices of the major unions in Australia. As you can see, the SDA easily has

more money than these four other unions combined.

In addition to the money held by the central office, the SDA

has significant funds held by their state branches and other offices. The

Victorian branch for example made its own profits of 1.56 and 2.37 million in

financial years 2015 and 2014 respectively, and has over 30 million dollars in

net assets. For NSW it’s harder to find up to date numbers as most financial

activity is funnelled through the interestingly named SDA NSW Deductions

Account Office, a separate entity that does not seem to have to report its

financial statements under the Fair Work act. Accounts lodged as evidence

during the Royal Commission into unions show the Deductions Account Office had

40 million dollars in net assets in 2013, and this amount could well have grown

substantially since then, with the organization reporting a cash surplus of 2.7

million during the 2015 financial year under disclosure laws for politically

related entities. When you add up the wealth of the various separate entities

of the SDA, there is easily more than 100 million dollars that has been saved

by the organisation.

The idea that the SDA has built this level of wealth while

putting together soft wages deals with the likes of Coles, Woolworths and

Hungry Jacks is distasteful. To put it another way, it means that a substantial

portion of these same members’ union fees were going to buying term deposits

for the SDA as opposed to genuine union expenses. Could the SDA have negotiated

better deals if they had spent more money by employing more people? Would more

representatives on the ground have allowed them to realize that their deals

were disadvantageous to some workers before Fair Work Australia pointed it out

to them? These are hypothetical questions, but reasonable given the events of

the last six months. The SDA might argue that by building up profits they are

ensuring the long-term life of the union, but most people joining a union would

reasonably believe that their fees are going towards the running of the

organisation, and not whatever empire building plan the union has in mind.

A couple of weeks ago, a rival to the SDA was announced, the

Retail and Fast Food Workers Union. Explicit in their criticism of some of the

SDA’s past practices, they are positioning themselves as a more progressive and

combative alternative. One of the main

things they are campaigning on is the reinstatement of penalty rates for those

workers that do not have them under SDA deals. While the SDA may not be

particularly popular, trying to build a union at a time like this will be a

difficult task. Union membership nationally has been declining, and the SDA are

well entrenched at many large employers. You would imagine the new union will

need a significant membership base before any of the larger companies agree to

even talk to them. Whatever the SDA’s reasoning for building up their balance

sheet to where it is now, one thing is clear: They have a significant war chest

to see off this latest challenge.